6 examples of PLG that went wrong (avoid their mistakes)

Discover the realities of Product-Led Growth (PLG): uncover why it's a challenging strategy, not suitable for all, through tales of success and failure in the complex world of PLG.

There's a lot of chatter around PLG these days. It's a deliciously enticing concept: streamline your sales cycle, let your product do the talking, and watch users convert themselves. But when you remove human interaction from the equation, the safety net vanishes.

You’re not the first person who wants to flip the switch on product led growth, and you won’t be the last. So, I thought it would be helpful to take you behind the curtains of a few companies who’ve bravely blazed a trail before us.

I’ve chosen the six examples in the post specifically for the lessons. You see, PLG is not always sunshine and rainbows (despite what you may assume from the behemoth top PLG companies). From false starts and poor timing to ill-informed assumptions, we have a lot to learn from when PLG motions don’t go to plan.

If you want to skip to the parts that resonate with you most, here’s a taste of what’s to come:

- Positioning backfired with SuveryMonkey vs Qualtircs

- Getting greedy with Amplitude

- Freemium implosion with Baremetrics

- Paid to free to paid with Outseta

- Dormant users with Equals

- Missed timing with Rdio

Let’s begin.

SurveyMonkey vs. Qualtrics: Clash of the growth models

On paper, SurveyMonkey had everything going for it: an amazing product, loyal customers, and a stellar team. But as you’ll soon discover, even with all the right ingredients, the very best-intentioned PLG strategy doesn’t always work out for the best.

To skip to the punchline, SurveyMonkey went public in 2018 valued at $2.6B, and Qualtrics IPO’d only a few years later at $16.5B.

So how did we get here? And where did SurveyMonkey’s PLG strategy go wrong?

Bottoms up vs top down (aka PLG vs PLS)

The fork in the road of this story began early on. While both tools inherently offer the exact same solutions, they took wildly different approaches to growth.

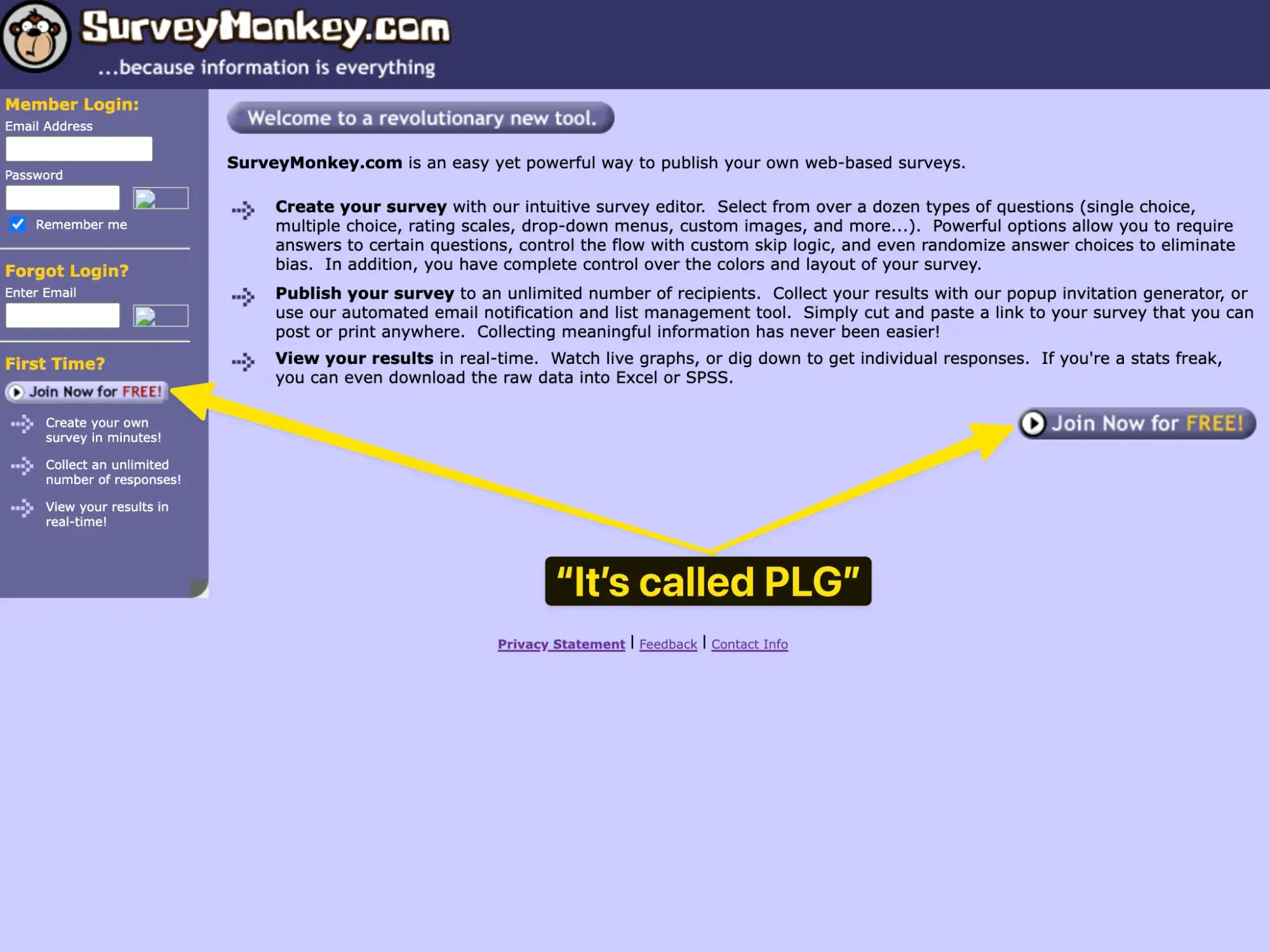

SurveyMonkey kicked things off with freemium self-serve from the get-go. This delightful trip down memory lane was snapped in August 2000 (yes, 23 years ago).

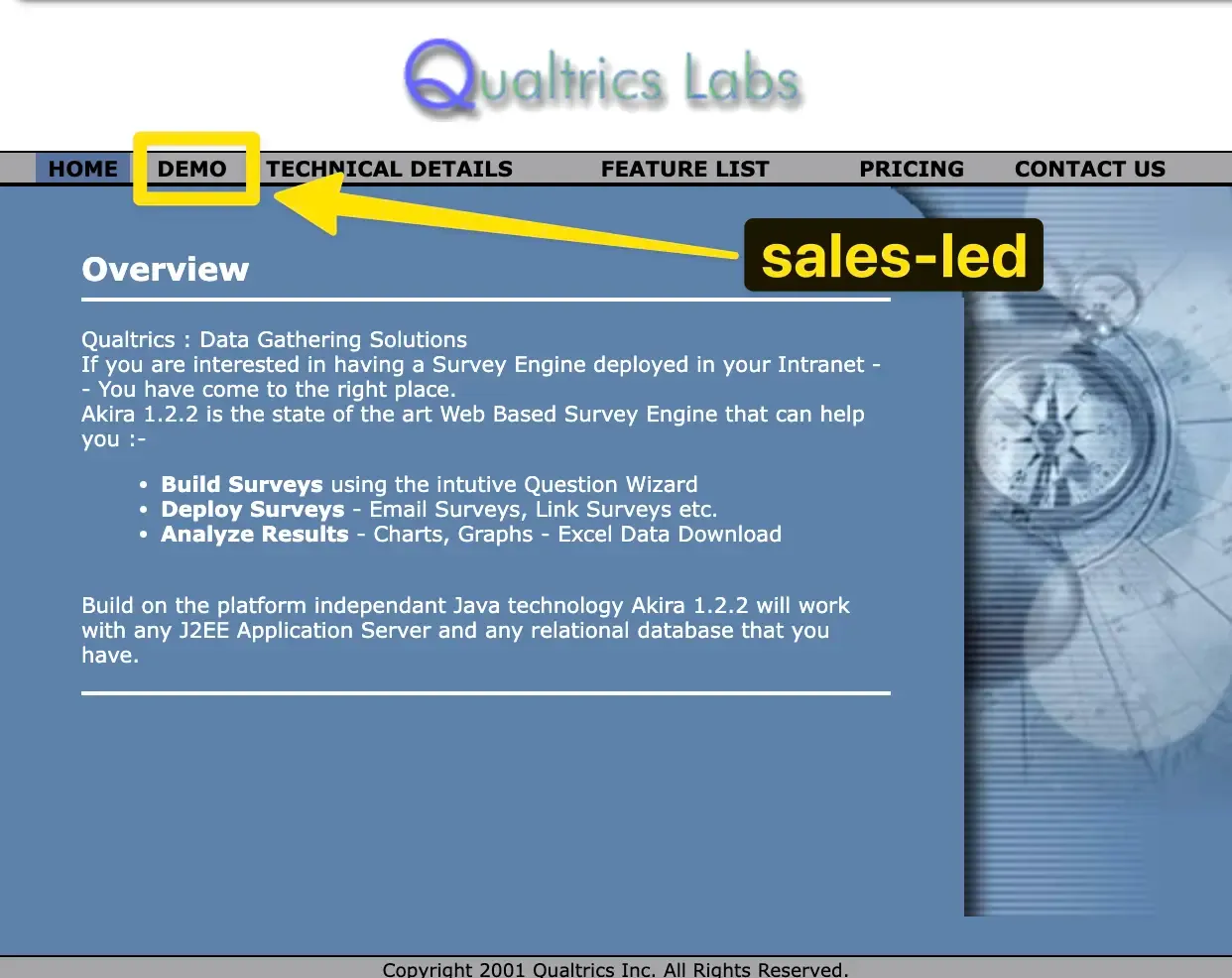

On the other hand, you have Qualtrics putting their sales-led efforts forward since October 2001.

You’ll also notice the positioning difference between these two almost identical tools: “web-based surveys” vs “data gathering solutions.”

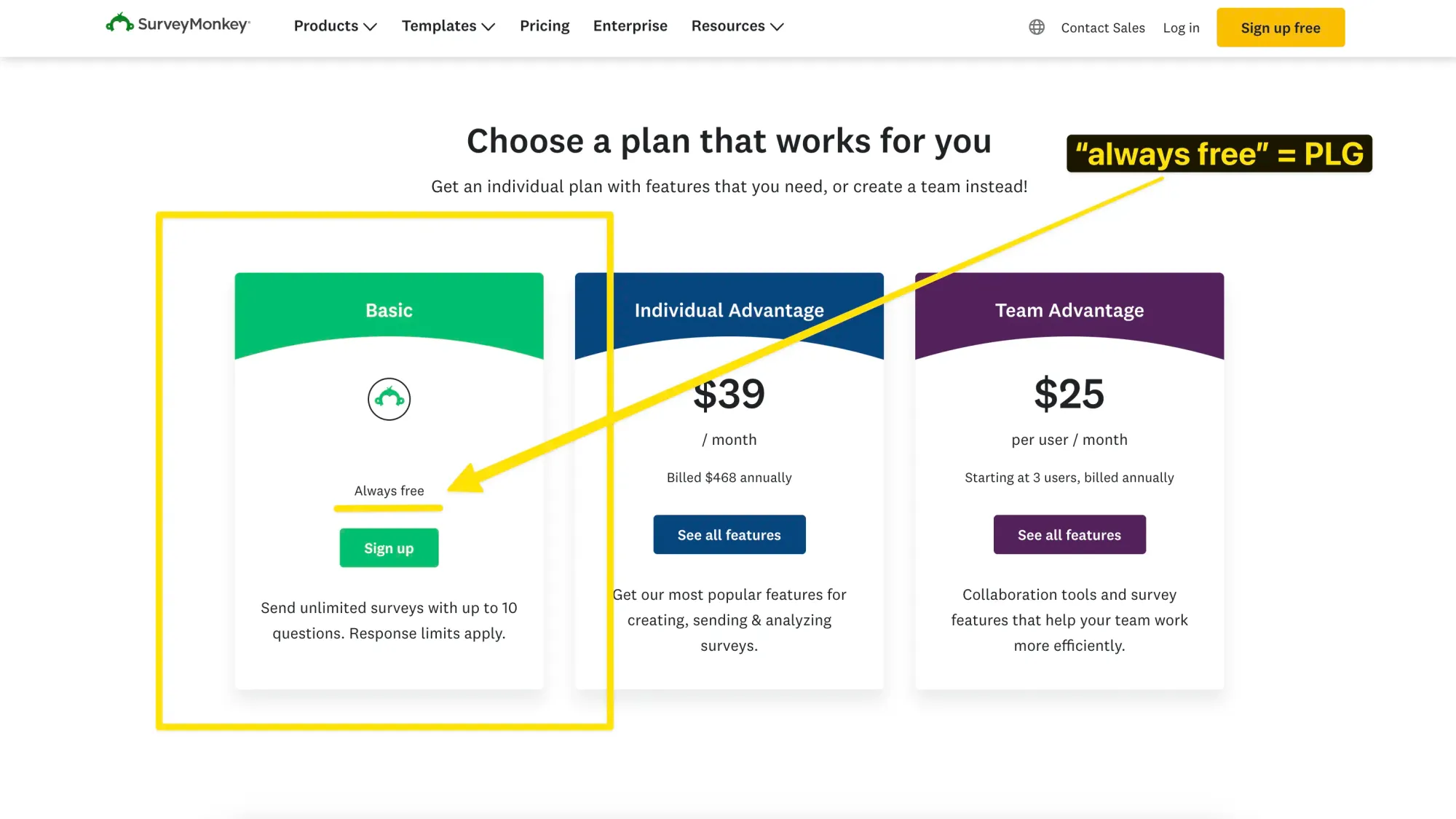

Fast forward 20+ years, and nothing has changed! SurveyMonkey is still running the freemium playbook.

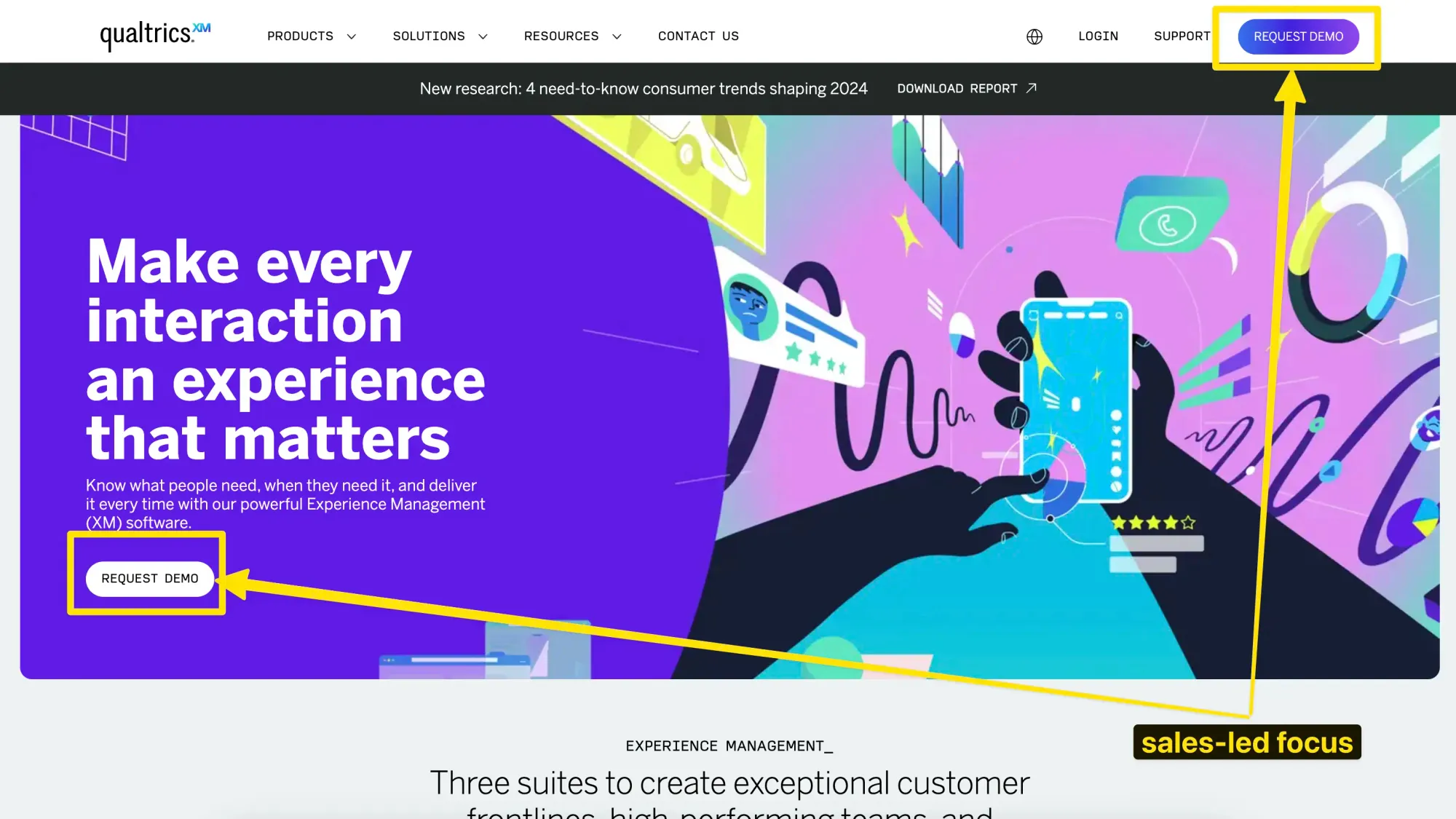

Qualtrics is still pushing hard along the sales-led path. They don’t even have a pricing page!

So why didn’t SurveyMonkey prevail as the leader?

By the time SurveyMonkey was attempting to capture the enterprise market, they still didn’t have their positioning dialed in. Take a peek at their 2013 website:

It was clear considering the growth that Qualtrics was experiencing that large organizations and teams didn’t want surveys, they wanted the analytics that surveys produce.

Ultimately, SurveyMonkey didn’t stand a chance.

- Their freemium offering was so valuable that 50% of their active users weren’t paying at all.

- There wasn’t enough of an incentive to push more adoption of paid features.

- Their positioning stifled their opportunity to enter into enterprise sales conversations.

Key lesson from SurveyMonkey vs Qualtrics

It’s hard to compete against a strong sales-led product with pure PLG.

Amplitude’s dependency on PLG temporarily stifles growth

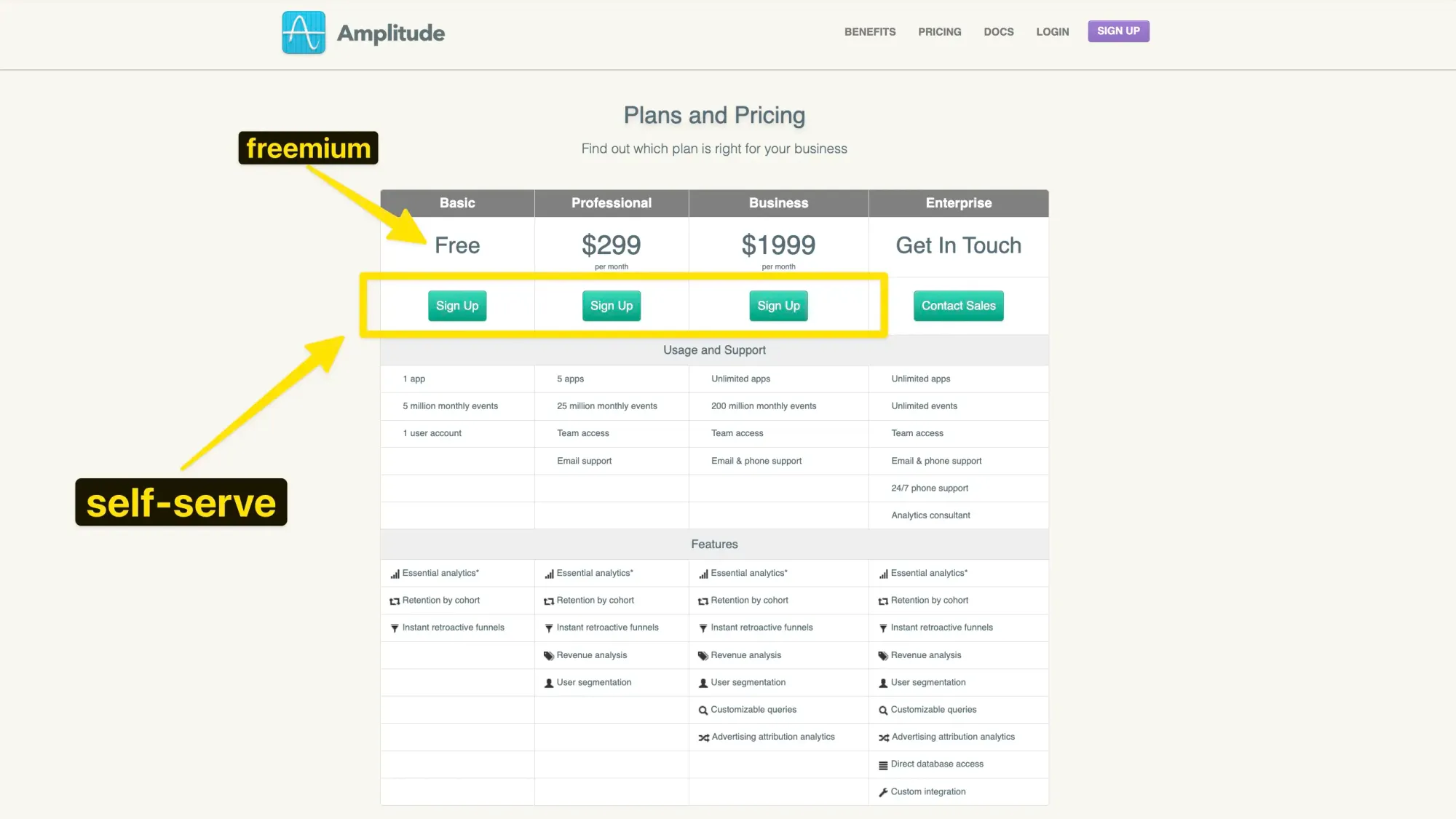

As you probably know, Amplitude is a meaty analytics platform focused on product, marketing, and experimentation.

Since August 2013 (see screenshot), Amplitude has been mostly running a PLG playbook. They’ve consistently kept a freemium model front and center and leaned heavily on their self-serve market to grow.

Still today, the company’s homepage nudges new users along a mostly unassisted acquisition model.

The turning point for Amplitude

However, one major insight that Amplitude caught early on was the fact that SMBs and mid-market companies were choosing their analytics tech stack based on how much they perceived the tool would scale with them as they grew.

This sounds like a no-brainer in hindsight, but in the moment, it was a compelling wake-up call for Amplitude. Their competitors were positioned as much more comprehensive and had “the logos” to prove it.

Ditching PLG for sales-led

Naturally, the company played catchup and pivoted to a primarily sales-led approach, amassing logos of some of the biggest Fortune 500 companies in the world. This was no tall order, mind you. Having relied almost entirely on PLG thus far, building out an entire sales force and upending their current growth strategies was disruptive.

The sales-led approach was undoubtedly successful, and the company eventually went public at a $5B valuation.

Reinstating the PLG model was a false start

Now that the foothold in the enterprise market was well solidified, the time had come to restart the PLG engine. They’d solved their biggest hurdle, positioning, and now it was time to capture the “budding growth companies.”

This is where the PLG waters get murky. According to former employees, the company hit three major hurdles at the time:

- Team dynamics: The primary concern from the sales team was that the newly relaunched self-serve options would cannibalize their sales pipeline, inevitably slashing commissions and reducing the salesforce headcount.

- Pricing doubts: They needed self-serve price points that were low enough that users would convert themselves without devaluing the much higher enterprise pricing options.

- Unhappy freemium users: The final nail in the coffin was the fact that while Amplitude had a large, thriving user base on their freemium tier, most of them weren’t using the product to its full potential. This meant that it was incredibly difficult to see the fruit of those product led growth flywheels.

To turn their PLG false start around, the team talked to as many non-converting users as they could to understand more about what was happening.

What they found was that users were seeing the pricing page and actively using the product but still not purchasing. It turns out that they were completely oblivious to most of the freemium plan’s limits or the tons of other features that Amplitude had on their paid tiers.

This is a good reminder for you to make sure your paid features are clearly visible to your free users in a way that is clean, accessible, and not overwhelming.

Another critical leak the team discovered in their PLG motion was a weak self-serve onboarding flow. Users were signing up and using the product but were completely overwhelmed with how to organize their analytics data.

Typically, in a sales-led approach, new accounts would have a dedicated onboarding specialist to walk them through setting things up. To rectify the situation, the growth team made significant changes around improving feature adoption, specifically implementing reverse trails for the paid features that were designed for managing data.

This turned out to be wildly effective in converting users into paying customers. Since then, Amplitude has successfully balanced a blend of PLG and sales led growth models, and they’ve continued to grow year over year.

Key takeaway from Amplitutude

You can’t always just flip a switch and turn PLG back on; your organization might have changed too much, making it harder to pull off.

At the brink: how Baremetrics narrowly escaped PLG induced implosion

Baremetrics is another analytics platform that almost crumbled under an ill-fated PLG strategy. Built entirely on top of Stripe’s API, they opted for up-front subscription payment plans from the get-go (see pricing table from 2014).

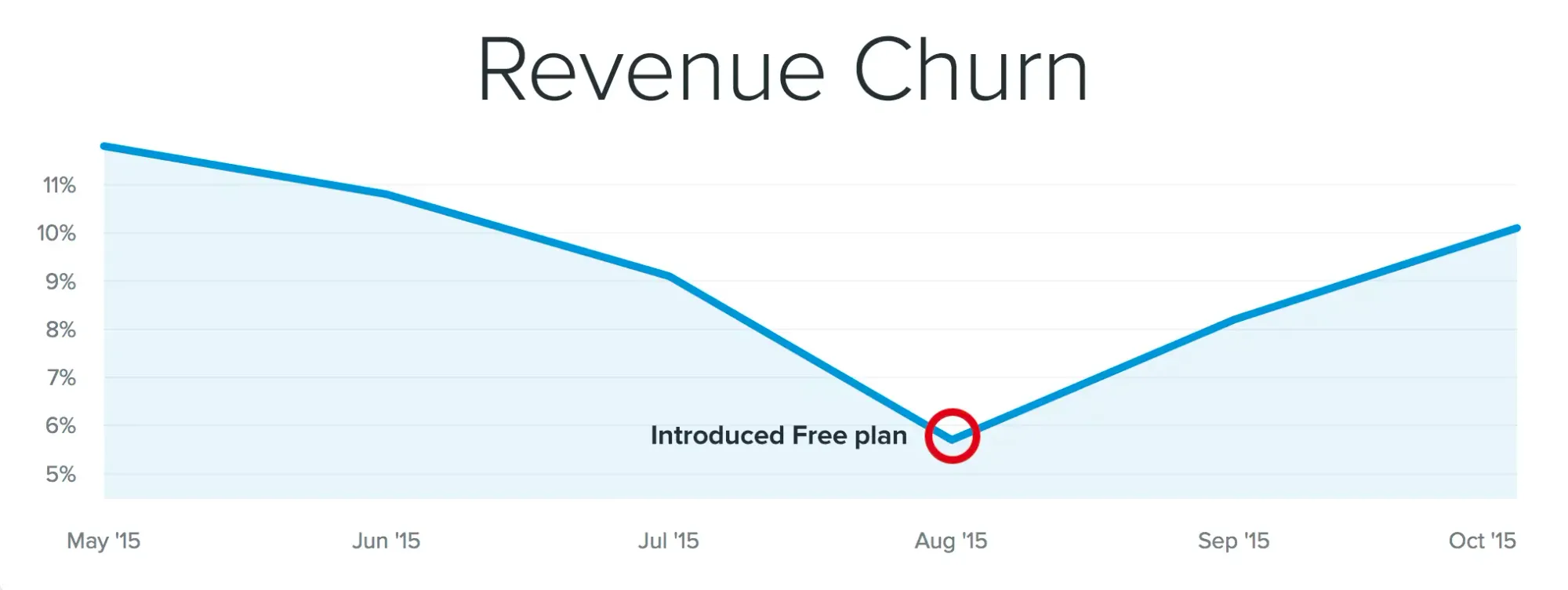

But in August 2015, they decided to switch things up in the search for growth and turned on their first freemium option.

The uptake of the free plan was a raging success. Over 1,000 new accounts signed up, and as (then CEO) and founder Josh Pigford puts it, “our “free” customers were outnumbering our “paying” customers, and the amount of data we’re both storing and processing had doubled.”

It became clear very quickly that the Baremetrics infrastructure could not handle the influx of accounts.

Because we have to pull down and store your entire data set from Stripe and then generate the metrics for every single day for every single plan on your account (and store that as well), there’s just simply a crap ton of data processing that happens. - Pigford, CEO

Stifling the implosion before it was too late

The overwhelm in processing data meant that the Baremetrics team was focused entirely on putting out fires just to keep the lights on. The user experience was buggy, unstable, and eventually completely unreliable - not just for the new free users, but for all users.

While Baremetrics was pulling in new users like crazy, they weren’t converting them into paid users, nor were they retaining their current customers.

Alongside that, their focus on stabilizing the platform meant they had no time to work on shipping new features or dedicating time to customer support and success.

The net result? Churn.

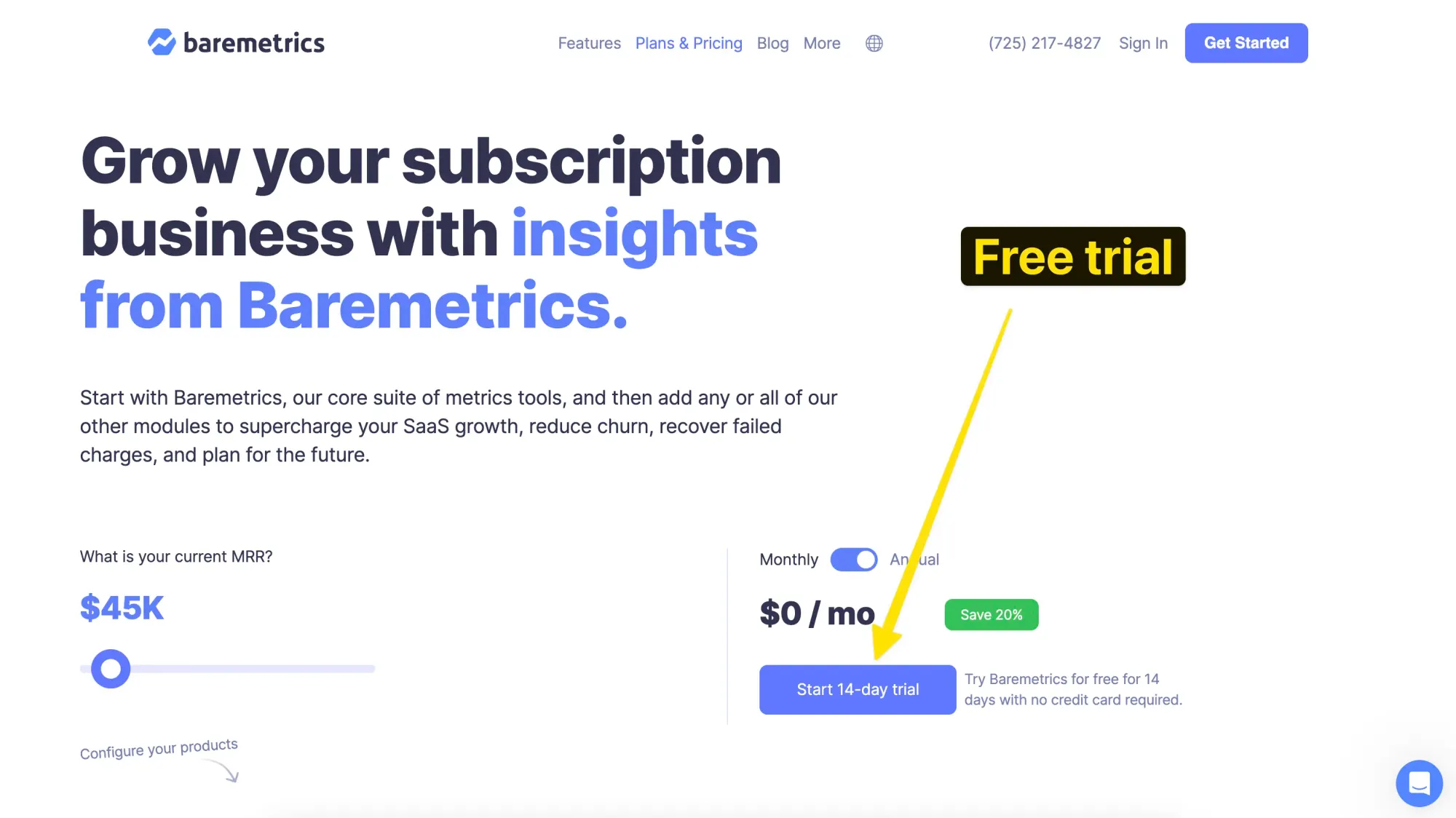

So, the plan instead was to switch to a free trial. Users would have full access to all paid features for 14 days. After that, they’d have the option to select a plan and continue. If they chose not to convert, their accounts would be sunset, and there wouldn’t be a technical load on Baremetrics.

This happy medium positioned the company well in 2 significant ways:

- There was now a cap on resource drain

- Revenue was more predictable & the team could scale accordingly

To this day, Baremetrics continues to offer a free trial as their primary growth lever.

Key takeaway from Baremetrics

Make sure you have the infrastructure and a solid conversion strategy in place before you implement your PLG motion.

The PLG gamble: Outseta's bold move and its aftermath

In the competitive world of membership platforms, Outseta sought to make its mark with an all-but-unique approach to product-led growth.

The idea behind their freemium offering was to create the ultimate, ideal customer experience. Users would sign up and be dazzled by the product’s free features, and as their business grew, they would inevitably upgrade to the more robust, paid features.

Biting off more than they could chew

The reality is that Outseta was fighting two simultaneous battles trying to keep this PLG strategy working.

The first battle was their target market. Aimed primarily at startups and budding new companies, the free plan was ideal. It would entice users onto the platform to support their new venture, but when their business didn’t take off or generate the expected revenue, they would stall and live on the free plan forever.

This meant the very small, bootstrapped Outseta team was supporting 1,000s of users with zero to no return. Which brings me to my next point.

The second battle they were fighting to keep the PLG dream alive was in supporting their users. Without proper onboarding, the tiny team was juggling customer support and success while trying to keep the lights on. There were no resources or time left to build new features or improve the product.

Free trial vs freemium strikes again

Not unlike what I’ve touched on previously in this post, Outseta also saw launching a free trial option as a great happy medium to replace their freemium offer. Again, for reasons we’ve just highlighted, this obviously brings a level of predictability and closure to the sales cycle.

Key takeaway from Outseta

Make sure your onboarding is dialed in and there is enough incentive or friction to encourage users to upgrade to your paid features quickly, especially if you're a small, bootstrapped team.

Equals' venture into uncharted PLG waters

Equals is the spreadsheet tool you’ve always wanted, but never knew you needed. Initially, they adopted a strategy of manually onboarding every individual customer to understand their use case and get to know them more. This subsequently helped the company gain a ton of traction and secure $16 million in Series A funding.

Pulling the trigger on PLG

From there, they barreled headfirst into their product led growth saga with the introduction of their now-infamous freemium model. The decision to abandon the hand-holding approach was largely influenced by other leading SaaS companies like Notion, Figma, and Airtable and their freemium models.

Build it, and they will come. But will they stay?

"Hoist open them gates, ye sea dogs!” With the onboarding call requirements cut and prices slashed, the free tier was a hit. A 4x increase in DAU should have been the signal to fire the confetti canons, but in reality, the situation was grim.

Churn was higher than ever, and the product really struggled to convert free workspaces into paid subscriptions. While a healthy amount of friction can be a good thing, in Equal’s case, it was just too hard for users to overcome:

- Create a workspace

- Connect data sources

- Invite team members

- Run queries

There are so many points in that user journey where they were hemorrhaging users. After six months of stagnation, the free plan was axed.

Long live the free trial

The resolution in this PLG false start was the introduction of a free trial to replace the free tier option. Naturally, this ever-so-gentle amount of healthy friction in the onboarding process helps to:

- capture higher quality users

- increase their level of commitment

- enhance perceived value (once inside the app)

- create urgency around feature adoption

To this day, Equals is still rocking with their free trial, and I personally don’t see any need for them to switch things up (at least for the time being.)

Key takeaway from Equals

Do not underestimate user journey complexity in a product led growth model. Missing the mark here will lead to high churn and tanked conversion rates.

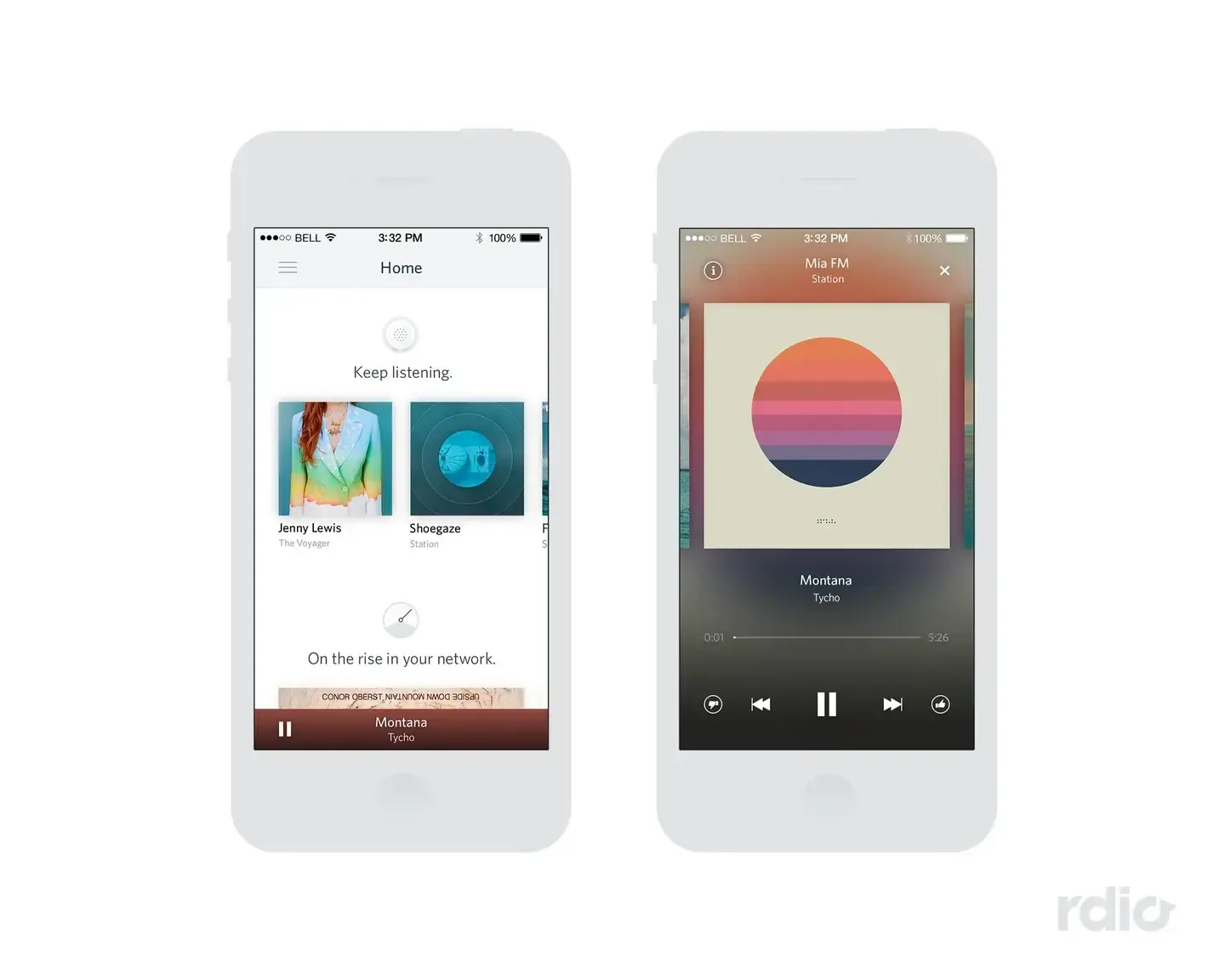

Rdio's illtimed PLG misadventure leads to demise

Imagine being the hottest music streaming app since sliced bread and so loved by users that there’s a cult-like aura emanating from your brand. Now imagine some little upstart company from Europe named Spotify sneaks in underneath you and wipes you off the map for good.

Rdio’s rise and fall is a classic example of misreading the writing on the wall. Spotify unlocked the hyper-growth lever early on in the music streaming game by opting for a freemium model. This strategy went against everything the market expected at the time. Music was always paywalled, and Rdio was playing by the rules.

This was their downfall ultimately.

By the time Rdio finally relented and launched a freemium option, their last-ditch effort to keep up with Spotify was too little, too late.

The hot take here for me is Rdio very well could have come out on top if they’d pushed PLG earlier. They had network effects dialed in and even a social graph baked into their product - something Spotify did not do at the time. It really was an unfortunate misjudgment of strategy to see such a promising product be eaten far too soon.

Key takeaway from Rdio

Be acutely aware of the subtle shifts in the market that you're in. Your PLG motion should be proactive in anticipation of market trends rather than reactive and too late.

Final thoughts

As we conclude this reminiscent waltz down memory lane, it's obvious that product led growth, while often a lucrative strategy, is not always the silver bullet of success for all companies. I hope the stories of SurveyMonkey, Amplitude, Baremetrics, Outseta, Equals, and Rdio have been useful for you to peek into the often-overlooked challenges of PLG.

In many cases, growth teams have pulled through, turned the ship around, and gone on to continue to grow incredible companies (while inherently serving countless customers of course). If there’s one way to summarize the takeaway from this post, it’s that PLG is a delicate balance of product excellence, market understanding, and timely adaptation.